Europe’s Fusion Champion Comes of Age: Proxima Fusion Raises €411 Million for Alpha, Its Net-Energy Fusion Demonstrator

HTGF and DTCF portfolio company Proxima Fusion has closed Europe’s largest-ever fusion financing round, a €411 million raise that values the company at €2.4 billion and marks a milestone for our Multi-Stage-VC platform.

Proxima Fusion, Europe’s leading stellarator company and the first spin-out from the Max Planck Institute for Plasma Physics, has been part of the HTGF and DTCF portfolio since its earliest days. Today’s announcement, a €411 million round led by XTX Ventures and East X Ventures, with RWE and Google as strategic investors, establishes Proxima as the best-funded fusion company in Europe. The investor base also includes Burda Principal Investments, Plural, UVC Partners, Balderton, Cherry Ventures, DST Global Partners, Brevan Howard Macro Venture, Lightspeed, DeepTech & Climate Fonds (DTCF), redalpine, Leitmotif, Elaia, CDP Venture Capital, Bayern Kapital,EIC Fund, KfW Capital and SPRIND. It is one of the largest private investments in European technology this year, and the largest ever in European fusion.

RWE became an investor just months after signing an agreement with Proxima to build the first stellarator fusion power plant on the site of a former nuclear fission power plant in Gundremmingen, Bavaria. Google’s investment underscores continued interest in fusion as a source of abundant, carbon-free, firm energy.

From research to industrial execution

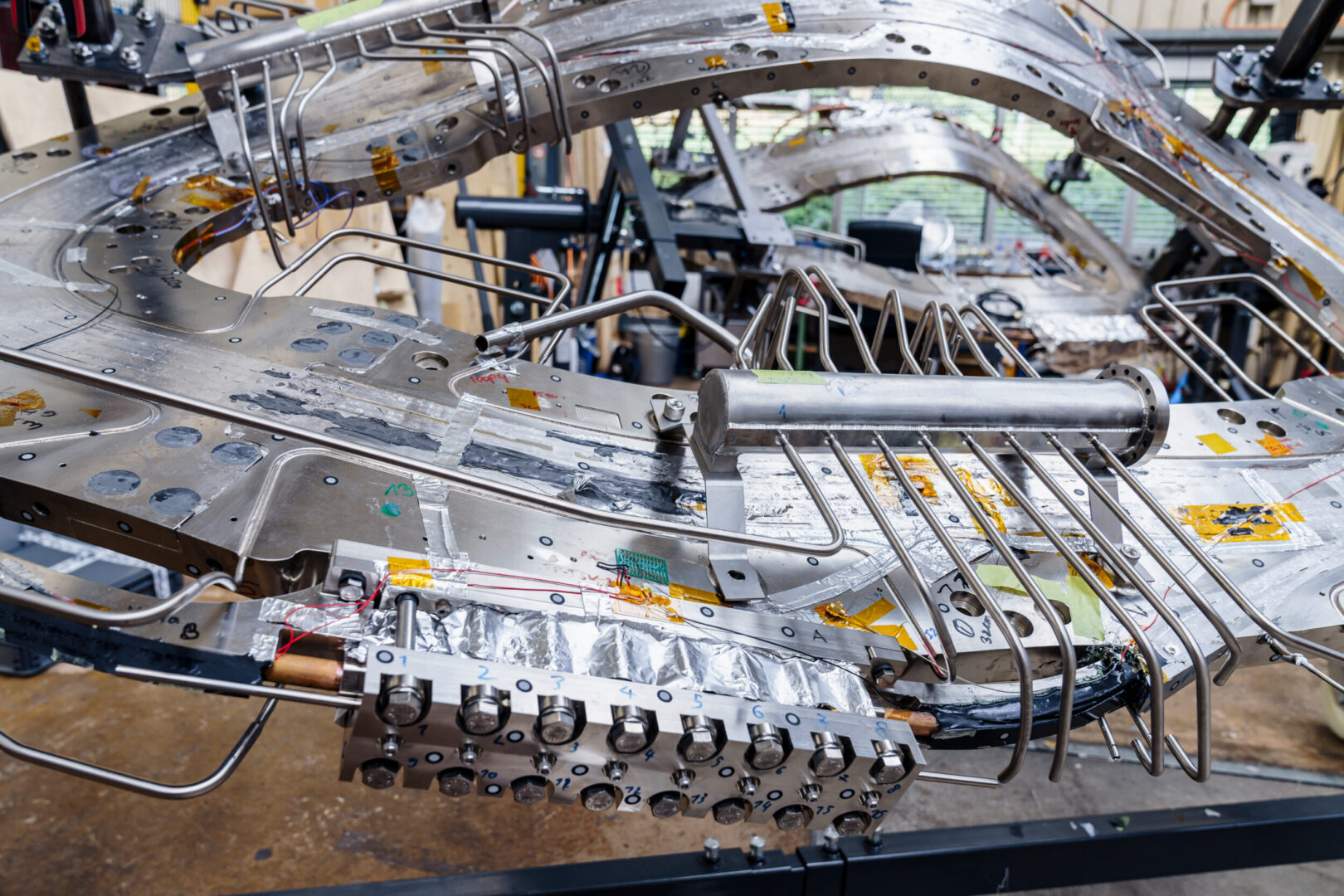

Proxima Fusion develops commercial fusion power plants based on its QI-HTS stellarator concept, building on the scientific breakthroughs of the Wendelstein 7-X programme. The financing funds Alpha, Proxima’s net-energy stellarator demonstrator near Munich, developed with the state of Bavaria, the Max Planck Institute for Plasma Physics and RWE. Alpha will validate key technologies and pave the way for Stellaris, the world’s first commercial stellarator fusion power plant.

“Europe is racing with the United States and China to get to the first fusion power plant. Proxima’s financing demonstrates that Europe can not only invent breakthrough technologies, but also build globally competitive companies around them,” said Dr. Francesco Sciortino, Co-Founder and CEO of Proxima Fusion.

In under three years, Proxima has secured more than €650 million, including €95 million in public grants. Just three months after signing its Memorandum of Understanding with Bavaria, RWE and the Max Planck Institute, Proxima completed this round, exceeding its target of matching Bavaria’s €400 million public funding commitment, showing how targeted public investment can catalyse private capital at scale.

With this financing, Proxima will complete the Stellarator Model Coil, expand HTS cable and magnet production, and accelerate hiring across its three locations in Germany, Switzerland and the UK.

Powering the New Wirtschaftswunder

We’ve supported this journey since the pre-seed phase in 2023, with DTCF joining at seed stage and playing a key role in the 2025 Series A. “I see hundreds of deep tech opportunities every year, and very few carry the weight of Proxima’s,” says Romy Schnelle, Managing Director at DTCF and HTGF. “When we backed Proxima at pre-seed, fusion was still a scientific ambition for most people. Only three years later, €411 million and investors like RWE and Google confirm it’s an industrial one. Recognising that shift early, and having the conviction to fund it, is what our Multi-Stage-VC platform is built for.”

“We backed Proxima from their very first round — not despite the ambition, but because of it,” adds Johannes Weber, Partner at HTGF. “Frontier deep tech that can spark a New Wirtschaftswunder in Germany and Europe is exactly what gets us out of bed in the morning. Proxima has a real shot at creating an entirely new industry and supplier ecosystem, with GDP-level impact. We couldn’t be prouder to be part of this journey.”

“This round shows that fusion is no longer a bet on distant science, it’s an investable industry today,” says Dr. Torsten Löffler, Investment Director at DTCF. “Proxima is proving that Europe has both the technology and the capital discipline to lead in one of the most consequential energy technologies of this century.”

Together, HTGF and DTCF pool more than €3 billion in fund volume to back founders seamlessly from first idea to international scale-up. Proxima Fusion is proof that Germany and Europe can build the foundation for a New Wirtschaftswunder, this time on fusion instead of coal and steel.

Press Release: Proxima Fusion Raises €411 Million to Build Europe’s Commercial Fusion Champion